15 Financial Independence Myths That may be Holding You Back

Pursuing Financial Independence is all about freedom—about regaining control over your life and aligning it with your interests and values. Photo by Matthieu Da Cruz on Unsplash.

Reading time: 9 minutes

Busting the Biggest Myths About Financial Independence

If you're new to Financial Independence (FI) or feeling overwhelmed by conflicting advice online, you're not alone. Despite its growing popularity, FI is still surrounded by confusion, half-truths, and outdated assumptions. Beyond myths, FIRE has also attracted criticisms—around privilege, market risk, and purpose. We addressed 20 of them head-on in a separate piece.

In this post, we’ll break down 15 of the most persistent myths about Financial Independence—like whether you need a six-figure income, own a home, or sacrifice all fun—to help you get started with clarity and confidence.

I’ve been on this journey for nearly seven years and writing about FI for close to three, so I’ve seen these myths come up time and again. Whether you're just exploring the idea or already on the path, today we’ll separate fact from fiction and show you how to make FI work for your life.

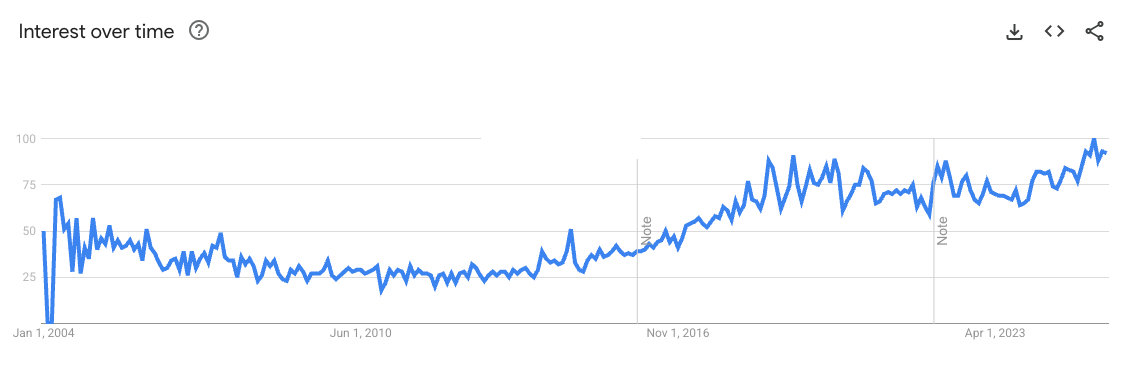

Interest in Financial Independence has skyrocketed in recent years. According to Google Trends, search interest in “Financial Independence” reached an all-time high in mid-2025 (Figure 1). What started as a niche personal finance concept discussed in early internet forums has grown into a global movement. Just the top few FIRE (Financial Independence, Retire Early) subreddits now have more than 4 million members combined.

It’s no surprise—nearly 80% of workers worldwide report being disengaged from their jobs. With rising dissatisfaction in traditional careers, more people are looking for ways to regain control, purpose, and freedom in their lives. Financial Independence offers a powerful framework to do just that—but only if you can move past the myths that often hold people back.

Figure 1: Relative interest over time (0-100) of the term “Financial Independence”. Source: Google Trends. As observed, in mid-2025 we reached the all time high.

20 Common Myths About Financial Independence—Debunked

1. You have to be rich or earn six figures to pursue FI

This is a very common misconception. Of course, it does help to have a higher salary to get to Financial Independence faster—all else equal, you will get there sooner with a $300K annual salary than a $80K take home pay. Some FI subreddits have been increasingly tilting towards a young, high-earning profile—and it’s usually this higher-earning profile that is also louder inside these forums.

The truth is, average earners can and do achieve Financial Independence every year. While having a high salary does make the pathway to FI easier, there are literally thousands of examples of individuals and families making it to FI on average salaries. In some cases, having a slightly above-average salary, combined with a low cost-of-living location and disciplined spending habits can get you to FI faster than a high-earning worker living in a very high cost-of-living area.

In the end, even with an average salary, you can make it to FI starting your investing journey early and being consistently disciplined over time—especially if you design your finances to be resilient and even antifragile, gaining strength from challenges instead of just surviving them. There is no reason you can’t make it there in your late 40s or early 50s.

You don’t have to have a top salary or be wealthy to pursue Financial Indepencence. Photo by Mitch on Unsplash.

2. Financial independence means never working again

Here we need to clarify the difference between FI and FIRE. The latter simply means having sufficient assets that allow you to live off their passive income over time, without depending on a paid employment. Financial Independence doesn’t mean quitting work—it means having the choice to keep working or not. In contrast, if you strictly follow the FIRE terminology (Financial Independence, Retire Early), you are stepping away from your career once you reach FI.

But that doesn’t mean doing nothing. Many individuals reaching FIRE continue to work in some capacity. As Vicky Robin said, “when we stop working for money, we may be out of a job, but we are never out of work”. The myth of early retirees lounging around all day couldn’t be further from reality—most fill their time with meaningful projects, travel, and personal growth.

Think about it. If you retire in your 30s or 40s, you still have 50–60 years ahead of you—are you really going to sit back and do nothing for decades? Of course not. Most of us will have to fill our time with different activities and interests that we enjoy.

Early retirement is often purpose-driven. Many FI folks go on to volunteer, write, start small businesses, or pursue creative and social projects. In fact, far from being an “escape”, pursuing FIRE can be a step deeper into life—reclaiming time, health, and purpose. While some early retirees may not earn a single penny ever again, my feeling is that the majority of young FIRE folk will continue to find new ways to contribute to society. Some of these endeavors will likely receive some form of monetary compensation.

Others may opt for “mini-retirements” or breaks between projects instead of one big final exit—treating FI more like a toolkit than a finish line.

Either way, the takeaway is that both FI and FIRE is more about gaining the freedom to choose how, when, and why you work. You work on your own terms, not on those of others.

Laying by the beach may sound great for a few weeks (or months), but if you retire in your 30s or 40s you’ll likely want to pursue other challenges too. Photo by Chris McClaveon Pexels.

3. FI is only for tech bros and finance nerds

One can be forgiven for thinking this. Open some of the popular subreddits, and there is a disproportionate number of posts from high-earning tech workers. Remember, though, that it’s human nature to enjoy flexing a bit in front of others—perhaps as a form of validation. Of course, this type of flexing will disproportionately come from high-income earners, not average income workers.

But keep in mind that some of the more frugal subredits have nearly as many members as their more spendy counterparts. For instance, the LeanFIRE subreddit, which seeks to “approach the problem of financial independence from a minimalist, stoic, frugal, or anti-consumerist trajectory” and suggests “retiring with less than $50K in planned yearly household expenses ($25k individual)” has 335,000 members—not bad.

In contrast, FatFIRE, which advocates for the entirely opposite philosophy, only has a slightly higher number of users—$445,000. The difference between these two approaches—LeanFIRE’s minimalist, frugal path and FatFIRE’s high-spending, luxury-oriented route—shapes not only how much you save, but also the lifestyle you build along the way.

Overall, as exemplified by these two ends of the spectrum, there is a lot of diversity in the FI community—nurses, teachers, scientists, small business owners, you name it—they are also there, not just the tech, finance, and healthcare workers. You don’t need a finance degree or an unusually high-income job to reach Financial Independence—just discipline and consistency.

Financial Independence is not only for workers in tech, finance, and healthcare. Photo by Danial Igdery on Unsplash.

4. FI means living like a miser and never spending on fun

One of the most persistent misconceptions about financial independence is that it requires extreme sacrifice—that you're condemned to a joyless life of rice, beans, and saying no to everything for a decade or two. Some FIRE folks do make this mistake. They urgently need to read Die With Zero—because life is about optimizing for fulfillment, not dying like a dragon hoarding gold in a cave.

That should be a myth—Financial Independence can still include joy, fun, and experiences. Remember that people pursue this path in the first place to increase their enjoyment of life. So, it’s important to distinguish between frugality and deprivation. As we’re reminded in Your Money or Your Life, frugality is about being intentional with your money—spending it only on things that bring you true joy—deprivation is about stripping out any joy from your life. The Financial Independence journey should embrace the former, not the latter.

At its heart, it’s a mindset of value-based spending. People don’t have to avoid spending altogether—they just choose to step away from what is expected from others and choose to spend it on what genuinely matters to them. For some, that might mean traveling often but not caring about having a large home, or it could be some who spends passionately on enjoying great food, but skips the latest tech gadgets. It’s not about cutting out the fun, it’s about cutting out mindless consumption and replacing it with intentional spending that reflects your values and long-term goals.

Pursuing Financial Independence doesn’t mean not spending at all, it means only spending on things that bring you value and joy. Photo by Priscilla Du Preez on Unsplash

5. Renting is throwing money away, so you must own a home

Many people have the deeply ingrained belief that renting is throwing away money and that true financial independence can only be achieved through home ownership.

But this idea doesn’t hold up under scrutiny. As explained by Ben Felix, when you compare all the real costs of owning—like interest, maintenance, property taxes, and lost investment opportunities—renting often comes out just as good financially. In fact, if you invest the money you save by renting, you can sometimes build more wealth than if you’d bought a home. This is particularly the case in some regions of Europe, where property prices near major cities are incredibly expensive relative to salaries.

Renting offers flexibility, mobility, and often far lower upfront costs, which can make it a smart choice for many people on the path to FI. I’m not giving universal advice here, because I’m aware this is a highly location and context-specific issue, but I’ve written before about how home ownership would really slow down my own path to FI.

While homeownership has benefits, it also includes costs that impact Financial Independence goals. When you buy a home, you tie up a large amount of capital that could otherwise be invested in income-generating assets. For some, that trade-off makes sense because it’s a lifestyle they want to pursue anyways, but for others it can slow their progress towards achieving financial freedom and any dreams they may have associated with it.

Financial independence isn’t about owning vs renting—it’s about designing a life that fits your values. Sometimes, renting is exactly what buys you the freedom to do just that.

Renting is not throwing money away—it can be a completely viable path to Financial Independence. Photo by Allison Huang on Unsplash.

6. Investing is too risky unless you're wealthy or an expert

Many individuals are afraid of the stock market and think you need a financial degree—or a lot of money—to invest safely. But today, this couldn’t be further from the truth. Thanks to some unsung heroes like Jack Bogle, investing has never been more accessible or beginner friendly. The idea of investing is not to become a stock-picking expert—you don’t need to time the market or study charts and company quarterly results all day. In fact, the data shows that long-term investors do best by keeping things very simple.

The easiest way to invest is to dollar-cost average (DCA) into low cost, internationally diversified index funds or ETFs that track them. A common misconception is that dividend-paying stocks are a safer or more reliable path to wealth—our article on dividend investing explains why total return indexing almost always serves FIRE investors better.

Investing in index funds allows you to buy small slices of the entire market on a regular basis, without trying to time the market. As Jack Bogle famously said, "Don't look for the needle in the haystack. Just buy the haystack." That’s what index investing is—buying the whole market and letting compounding do the heavy lifting over time. You get instant diversification, minimal fees, and solid long-term performance.

Staying invested is crucial for long-term Financial Independence success. History shows that patient, low-cost investing beats most active strategies. Even missing just a few of the best days in the market can wreck your returns—so timing the market is a fool’s errand. This holds even through the most extreme events—such as geopolitical conflict and war. Assuming you’re portfolio is well diversified, you would have recovered from every single one of them.

You don’t need to be wealthy to get started, even small, regular contributions grow over time. In fact, the best thing is to start out small when you are young, which provides you with the opportunity to build the behavioral investing muscle early on. Bogle’s philosophy—own the market, keep costs low, stay invested—works whether you’re investing €50 or €5,000 a month. It’s not about beating the market. It’s about making sure you don’t lose to fees, emotion, and complexity.

Investing can look complex from the outside, but it doesn’t have to be. For most retail investors, consistent investing into low-cost, internationally diversified index funds and holding them for the long run will do the trick. Photo by Nick Chong on Unsplash.

7. You can’t pursue FI if you have kids

As illustrated by thousands posting across different FIRE subreddits, having children doesn’t disqualify you from pursuing financial independence—it just changes the parameters of the journey. As we’ve written before—illustrating our own example as case-study—the path to FI path with kids will be slower, but still completely possible, and, of course, more meaningful to those who want a family. The key is adjusting your timeline and priorities—not to give up on the goal.

Children do bring additional costs, but they can also become part of a more value-driven lifestyle. In fact, for some, they can be the very reminder you need to make sure you enjoy the journey, not just reach the destination a couple of years sooner. When you look back in old age, it won’t matter whether you reached FI in 12, 14, or 20 years—what will matter in the end are the memories made and the fulfillment experienced.

Also keep in mind there are many ways to raise kids, and these vary dramatically in different locations. Many FI families raise their kids with an emphasis on quality time, shared experiences, and mindful spending rather than material consumption. That alone can make a tremendous difference over time. In our case, having one kid barely made any impact on our FI numbers. Having three though most certainly did: as we discuss in a dedicated post, although we keep most of common expenses in check, upgrading to larger living arrangements did substantially increase our monthly expenses.

Financial independence is about designing a life that works for you, kids included. If you want to have kids but worry about your FI journey… well, please stop this silly thinking already!

Enjoy the ride, not the destination. It’s completely possible to pursue Financial Independence while growing a family. Photo by Jessica Rockowitz on Unsplash.

8. Pursuing FI will ruin your career prospects

A common fear is that pursuing Financial Independence means stepping off the traditional career path immediately—and damaging your future prospects in the process. But, for most, FI really does the opposite, it gives you leverage during your career. When you’re not financially dependent on your next pay check, you start making decisions from a position of strength, not out of fear.

Pursuing Financial Independence means you’re in a stronger position to walk away from toxic jobs, negotiate better terms, or take high-upside potential career risks that other peers wouldn’t be able to stomach. I recently wrote about how I stepped away from my conventional job several years before reaching FI: being well on the path to FI made me question why I should wait to start designing a more meaningful, less stressful life.

As with my case, many people on the FI path actually find themselves moving into more meaningful, aligned work—whether that’s switching industries, going part-time, or launching their own business. When money stress is out of the equation, you're suddenly free to opt for purpose over career status, creativity over politics. In a nutshell, FI doesn’t end your career—it gives you the power to shape it.

In most cases, pursuing FI will make you a more valuable worker. Photo by ThisisEngineering on Unsplash.

9. You’ll be bored once you reach financial independence

Many individuals are used to structuring life around work, so the idea of stepping away from a job can feel like stepping into a void. What would I do all day? Wouldn’t I lose my sense of purpose? These are natural concerns to have—after all, with so many years practicing the same routine, it can feel scary to make any change. Most of us are creatures of habit.

Although the concern is valid, it’s usually based on the assumption that work is the only source of identity and fulfillment possible. But remember what we mentioned earlier—data shows that almost 80% of the global workforce don’t find fulfillment in their jobs. So what is it exactly you are scared of leaving behind? Are you sure you need your boss and her goals to find structure in your day?

Perhaps it’s simply that we’ve lost the ability to think outside the box. When we were kids and teenagers we were teeming with creativity—we had all kinds of ideas and dreams we wanted to fulfill when we grew up. So off we went to get a job, earn some money, and try to fulfill some of them. But somehow along the way we completely forgot about those dreams and that the job was a means to an end, not an end in itself. Instead, we started playing the work and money games for their own sake—to pursue a high income and a prestigious title that others might approve of.

In reality, FI creates space—space rediscover passions, develop creative projects, travel, volunteer, or simply enjoy more time with loved ones. Reaching Financial Independence often increases fulfillment, purpose, and time for passion projects.

Another day I will write a post on all the ideas I have for my post-FI phase, which I’m sure will continue to evolve over time as life changes. But, for the moment, suffice to say that if we can’t think about what we’d like to do it’s because we’re running on autopilot.

A common misconception is you will be bored all day after reaching Financial Independence. Perhaps you have just been to centered in your career—there is so much to explore and learn in life. Photo by Ross Sneddon on Unsplash.

10. FI requires obsessive budgeting and complex spreadsheets

It’s fairly common to assume that everyone on the path to FI has a perfectly color-coded spreadsheet and tracks every cent. And while FI does seem to attract detail-oriented folks that enjoy optimizing, you definitely don’t need to track every expense to be successful at FI. Different people use different systems—what matters most is finding one that works for you.

When first starting out on the FI journey, I would recommend following Vicky Robin’s classic Your Money and Your Life advice—definitely read the book if you haven’t already. Tracking your spending in detail is exactly what will enable you to make value-aligned decisions on how to improve your savings rate and accelerate your path to Financial Independence.

But once you are optimized, you will develop a sense of whether your spending is aligned with your objectives or not. If you choose to not record single expenses and only what goes in and out every month, that’s fine. Again, the important thing is that your spending is truly aligned with what brings you joy in life—that you are not just spending for the sake of it or to conform with others’ values.

I’d recommend following a pay-yourself-first budget, irrespective of whether you track every single expense or nothing at all (or something in between). In doing so, you automatize your investments (and savings rate) at the beginning of the month. The rest of the month you can spend freely your remaining salary.

Either way, the key to FI is consistency over time over perfection. It’s about aligning your money habits with your long-term goals. Financial Independence means freedom to live intentionally, not obsess over every transaction.

Create a system that works for you and stick with it. It doesn’t have to take more than 30 mins each month to track your spending. Photo by Campaign Creators on Unsplash.

11. FIRE doesn’t work in Europe or outside the U.S.

I’m an expat currently pursuing FI in Germany, so I can assure you it’s definitely possible. Even with three kids and working part-time. As mentioned in our first point, of course you will find higher salaries in other countries, e.g. the US, Switzerland, Singapore, and others.

But remember that income is just one part of the equation and that many high spenders often face disproportionally high costs and don’t necessarily end up with a high savings rate—the most important lever on your path to FI. To illustrate, schooling is free in Germany and childcare incredibly affordable. Moderate salaries with a relatively affordable cost of living also works.

The best locations to pursue FI are those that have a good salary to cost-of-living ratio. We recently published a ranking of the top 10 best locations to move abroad to accelerate FI—so, of course, location matters. But as country-based subreddits suggest, Financial Independence is something people are pursuing all around the world, not just in the US. For a Europe-specific breakdown, we also ranked the best European countries to work in to maximise your savings rate.

There are also some advantages of pursuing FI outside of the US. To illustrate, many FI/FIRE folks outside of the US won’t have to deal with their US counterparts’ headaches when it comes to healthcare—it will continue to be affordable and high quality in retirement. Similarly, there are many social safety nets that make the path to FI less risky in Europe than in the US and other countries, despite the lower salaries.

Lisbon, Portugal. Portugal ranked as the best place to retire in Europe, but, of course, it is not the most optimal place to live on the accumulation phase of FIRE. We developed a ranking for the top countries globally to pursue FI during the accumulation phase.

12. The 4% rule is guaranteed in all situations

The 4% rule is often quoted like gospel by many in the FI community. And, indeed, as we’ve covered extensively in this blog, it can be a very useful rule of thumb when used appropriately. But we shouldn’t see it as a guaranteed outcome, especially for early retirees considering 40 or 50+ retirement timelines.

The bottom line is that we should stay aware of market conditions and monitor how our portfolio is performing. This doesn’t mean to attempt to time the market and buy and sell aggressively, but to adjust out spending if needed. Flexibility is key here.

If you’re interested in safe withdrawal strategies that work even better than the 4% rule (or the recently updated 4.7% rule), we recently wrote about dynamic spending strategies like the Variable Percentage Withdrawal (VPW), the Guardrail Withdrawal Strategy (GWS), and/or the bond tent method.

These are all good places to start if you want something safer than following fixed spending rules like the 4% approach. Always remember to consult your plans with a financial advisor that can confirm a strategy based on your unique circumstances.

Although the 4% rule (of thumb) should be used with care, early retirement math doesn’t have to be difficult. Photo by Thomas T on Unsplash.

13. You must have a side hustle to reach financial independence

Many YouTubers will have you think that having a side hustle is key to Financial Independence. And they are correct in the sense that it will accelerate your timeline to FI—but at what cost? Again, tying with the main themes of Die With Zero, we are trying to optimize life for fulfillment, not to reach FI two years sooner.

Nobody is keeping a record of how fast you get there—nobody is clapping for you at the finish line. In fact, nobody cares. What’s really important is that you enjoy the ride.

Some of the side-hustle examples you see online—especially from people with young kids—are frankly mind-boggling. You’re pursuing FI arguably to have more control over your lifestyle and spend more time with your loved ones, yet decide to sprint to the finish line by trading your time with them. This is an example where delayed gratification simply doesn’t work so well.

Side hustles are trendy but certainly not a requirement. Many people reach Financial Independence with no extra income streams at all—just by saving a high percentage of their salary and investing consistently. Pushing too hard with side hustles can lead to burnout, especially if you're already working a demanding job. Keeping fixed expenses low and automating investments can be more sustainable than chasing endless hustle.

A side hustle can help, but it generally not required and can even lead to burn out and frustration on the path to FI. Slow and steady wins the race. Photo by JavyGo on Unsplash.

14. You can't reach FI if you’re starting late

Starting your FI journey in your late 30s or 40s might feel “too late,” but it’s far from impossible. Plenty of people build financial security in just 10-15 years by combining higher late-career earnings, reduced expenses, and focused investing.

Also, remember than in many places, e.g., Europe, conventional retirement continues to be pushed back further and further (e.g., 70 years in Denmark, other countries soon to follow suit). Even if you did come across FIRE with no savings at age 50, chances are you can still turn your situation around by following FI principles. After all, you were headed to a retirement in poverty.

Yes, compound interest has less time to work, but compound discipline matters just as much. Later in life you can consider as well other possibilities, e.g., downsizing and reinvesting your home equity or relocating to a lower cost-of-living location—we recently wrote about the huge benefits of geographic arbitrage and early retirement when relocating abroad.

It’s never too late to take control of your finances. Reaching FI late is still reaching freedom. What matters most isn’t your starting point—it’s your willingness to change direction.

It’s never too late to start your FI journey. Photo by Rana Sawalha on Unsplash.

15. Early retirement means being lazy or unambitious

Many people equate early retirement with sipping piña coladas by the beach—sitting around and doing nothing. While this may be the case for some—especially older early retirees—for most of the FI community it’s likely the opposite.

Many early retirees become entrepreneurs, start creative endeavors, or work on improving their community in some capacity. We’ll all continue to “work”—it just means we will choose what to do without needing to earn a paycheck.

Pursuing Financial Independence is not about escaping work or life. It’s about removing the pressure or need to monetize everything and to live life on someone else’s terms. When money is no longer the main driver, people often become more ambitious, not less, pouring their time into meaningful projects, side ventures or passion-driven work. It’s not laziness—it’s freedom to design your life and contribute on your own terms.

Final Thoughts: Redefining the Path to FI

Reaching financial independence isn’t about following a rigid formula or meeting someone else’s timeline—it’s about creating a life that aligns with your values, priorities, and unique circumstances, and ensuring it’s not just resilient to setbacks but positioned to benefit from them.

Whether you're starting early, late, with kids, or without a side hustle, the path to FI is still available—and it’s more flexible than most people think, partly because you can choose anywhere along the FI spectrum, from the stripped-down efficiency of LeanFIRE to the more expansive comfort of FatFIRE, depending on your goals and lifestyle preferences.

We’d love to hear your perspective. Are you navigating any of these myths in your own journey? Share your thoughts in the comments, and feel free to pass this post along to someone who might need a mindset reset around FI! Your story might just help someone else take their first step.

🌿 Thanks for reading The Good Life Journey. I share weekly insights on money, purpose, and health, to help you build a life that compounds meaning over time. If this resonates, join readers from over 100 countries and subscribe to access our free FI tools and newsletter.

👉 New to Financial Independence? Check out our Start Here guide—the best place to begin your FI journey.

If you enjoyed today’s post, I think you’ll also enjoy our article covering alternative approaches to traditional FIRE—Barista FIRE and Coast FIRE—or our post on cutting your FIRE timeline by 10 years thanks to geographic arbitrage. Didn’t find what you were looking for? Check out our most recent articles further below.

Disclaimer: I am not a financial adviser, and the content in this website is for informational and educational purposes only. Please consult a qualified financial adviser for personalized advice tailored to your situation.

Check out other recent articles

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Frequently Asked Questions (FAQs)

-

No. While high income can speed up your progress, many people achieve Financial Independence on average salaries. The key is maintaining a high savings rate by controlling big expenses—like housing and transportation—not necessarily earning six figures.

-

Description text goNot at all. FI simply means having enough assets to choose whether or not to work. Many people continue working in meaningful ways—freelancing, volunteering, or starting businesses—once they reach FI. It's about freedom, not early retirement for everyone.es here

-

Yes, absolutely. Having children may slow the path slightly, but many families still reach FI by focusing on value-based living, optimizing big expenses, and planning intentionally. FI is flexible enough to include family goals and priorities.

-

No. While tracking expenses can help early on, it’s not essential long-term. Many people use the 80/20 rule—focusing on the biggest costs—and automate their savings and investments without obsessing over every coffee or small purchase.

-

Yes. Even a 10–15 year FI path is realistic if you’re focused and intentional. Late-career earnings, reduced lifestyle inflation, and options like downsizing or relocating can help build wealth, even if you didn’t start young.

-

Not necessarily. Renting can offer lower upfront costs, more flexibility, and the ability to invest the difference. In high-cost real estate markets, renting while investing elsewhere can be smarter than owning an overpriced home.

-

No, it’s a rule of thumb—not a guarantee. Market volatility, inflation, and your spending flexibility all matter. More adaptive strategies like the Guardrails or Variable Percentage Withdrawal method can provide better safety for early retirees.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles: