7 Effective Budgeting Strategies to Reach Financial Freedom

The right budgeting system turns financial chaos into clarity and creates the headspace to actually pursue Financial Independence. Photo by Workperch on Unsplash.

Reading time: 12 minutes

Quick answer — Which budgeting strategy is best for Financial Independence?

The combination of Pay Yourself First (#5) and Zero-Based Budgeting (#4) works best for pursuing Financial Independence (FI). Pay Yourself First ensures savings happen before any spending decisions have taken place, while Zero-Based Budgeting gives every remaining dollar a deliberate purpose. Together they turn saving from passive to intentional—the key shift that accelerates your path to FI. The 50/30/20 method is a solid starting point for beginners but a 20% savings rate will take around 30 years at a 7% real return—roughly a traditional retirement timeline, not an early one.

What you'll get in this article

✔ 7 budgeting methods explained with pros, cons, and real examples

✔ How each method aligns with pursuing Financial Independence (including ratings)

✔ Why savings rate matters more than income or stock market returns

✔ A comparison table of all 7 methods at a glance

✔ The recommended combination for FI-focused budgeters

✔ A decision framework to find the right method for your situation

✔ FAQ targeting the most common budgeting questions

TL;DR — 7 Budgeting Strategies 💰

🥇 Best for FI: Pay Yourself First + Zero-Based Budgeting combined

📊 50/30/20 is popular but a 20% savings rate takes 30+ years to reach FI

✉️ Envelope budgeting gives spending control but doesn't prioritise saving

🔢 Traditional budgeting treats savings as what's left over—too passive for FI

📱 Digital apps are tools, not strategies—it’s possible to pair with a specific method

🎯 The key shift: from "save what's left" to "spend what's left after saving"

⭐ FI ratings range from ⭐⭐ (passive) to ⭐⭐⭐⭐⭐ (intentional)

At a Glance: 7 Budgeting Methods Ranked for Financial Independence

| Method | Saving Approach | FI Rating | Best For | Main Weakness |

|---|---|---|---|---|

| Traditional | Save what's left | ⭐⭐ | Beginners needing basic control | Savings is an afterthought |

| Envelope | Control spending by category | ⭐⭐ | Overspenders in specific categories | Doesn't prioritise saving |

| 50/30/20 | Fixed 20% to savings | ⭐⭐⭐ | Stepping stone for new savers | 20% too slow for early retirement |

| Zero-Based | Every dollar assigned a purpose | ⭐⭐⭐⭐ | Detail-oriented FI pursuers | Savings not guaranteed first |

| Pay Yourself First | Save first, spend the rest | ⭐⭐⭐⭐⭐ | Anyone serious about FI | No framework for remaining spend |

| Percentage-Based | Fixed % to each category | ⭐⭐⭐ | Variable income earners | Percentages may not be aggressive enough |

| Digital Apps | Track spending automatically | ⭐⭐ | Support layer for any strategy | Tool not strategy — tracking ≠ saving |

Why Your Budgeting Method Determines How Fast You Reach Financial Independence

Most people budget the wrong way—they spend first and save whatever's left. It sounds harmless, but this single habit is one of the main reasons people never reach Financial Independence (FI). It’s no wonder they find it difficult to save with this approach. This passive strategy is built on the flawed assumption that what remains after all your expenses have been covered will somehow provide financial security over time.

Unfortunately, “whatever is left” is usually not enough to reach Financial Independence or early retirement in any reasonable timeframe. Worse, it may leave you in retirement without enough savings. In a world where lifestyle creep, subscription services, and spending pressure amplified by social media, what’s left tends to be very little—or nothing at all.

This is the single most important insight in this article: there is critical difference between “save what’s left” and “spend what’s left after saving.” These two approaches sound similar, but produce very different outcomes over time. The first method makes saving an afterthought, while the second one makes it a non-negotiable.

This article compares 7 common budgeting methods, explains how they work in practice, and ranks them by how well they support the goal of reaching FIRE (Financial Independence, Retire Early) faster.

If you're here for a quick answer, the comparison table after the TL;DR gives you all 7 methods at a glance. If you want to understand why the method matters—and see the FI timeline impact in numbers—the full article covers both.

👉 If you're new to Financial Independence, start with our complete guide to Financial Independence.

Most people are sitting on unoptimised spending without realising it. The right budgeting method surfaces it. Photo by Cottonbro Studio on Pexels.

Why Savings Rate — Not Income — Determines Your FI Timeline

Before we start comparing different approaches, it’s worth anchoring the discussion around the single most important variable in FI planning: your savings rate.

Your savings rate is the percentage of your net (after-tax) take-home pay that you consistently save and invest each month. Critically, its relationship with the time it takes to reach FI is not linear—the early gains are disproportionately powerful. As observed in Figure 1, moving from a 10% to a 15% savings rate can reduce your working career by almost 9 years, while the same incremental effort from 50% to 55% may only provide an additional 1-2 years.

Figure 1. The non-linear relationship between savings rate and years to Financial Independence. Small improvements in savings rate—especially in the 0–30% range— produce disproportionately large reductions in working years.

The good news for poor savers is that wherever you’re starting from, even a modest improvement in savings rate is likely to produce an outsized reduction in the length of your working career. Indeed, the lower your current savings rate is, the more dramatic that reduction will be.

The relationship between savings rate and FI timeline is non-linear for a specific reason: as you increase your savings rate, two things happen simultaneously. First, you invest more each month—so your portfolio grows faster. Second, and less obviously, you also reduce the total portfolio you need to retire, because a higher savings rate means lower monthly expenses, which means targeting a smaller FI number.

It’s important to let these numbers sink in. Going from a 10% to a 20% savings rate isn’t just measured as a 10 percentage point increase, but holds the potential to retire 15 years earlier.

This is why your choice of budgeting method matters so much: the right approach can systematically raise your savings rate by 10, 15, or more percentage points without requiring in many cases dramatic lifestyle sacrifices.

This aligns with research from Vanguard's How America Saves report, which consistently shows that households with automated savings contributions outperform those who save manually—regardless of income level.

The numbers above feel a bit abstract until you apply them to a real household. Here's what the difference looks like in practice.

Case Study: What Switching Budgeting Methods Did to One Household's FI Timeline

Consider a household with the following profile:

Age: 35

Net annual household income: $80,000

Current annual expenses: $72,000 (savings rate: 10%)

Current portfolio value: $50,000

Assumed real return on investments: 7%

Safe withdrawal rate: 4%

Under a passive Traditional Budget—saving whatever is left over—this household saves roughly $8,000 per year. According to our FI Calculator, they would reach Financial Independence in approximately 36 years, having to wait until age 71 to fully sustain themselves from their investment portfolio.

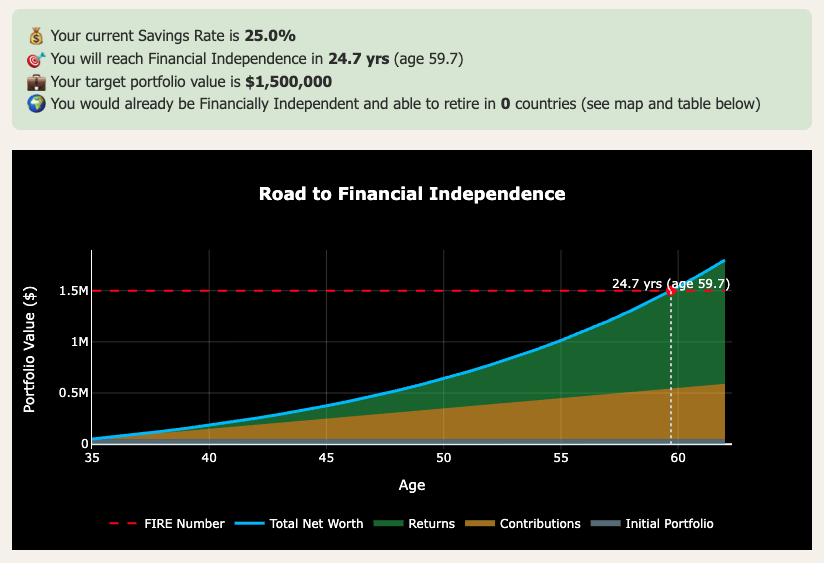

Now consider they switch to a Pay Yourself First + Zero-Based Budgeting—both explained in the following sections of this article. By automating savings at the start of the month and deliberately allocating the remainder, they manage to raise their savings rate from 10% to 25%—saving $20,000 per year instead of $8,000. Without earning a single dollar more, their FI timeline drops to approximately 25 years—a difference of nearly 12 years of working life (Figure 2).

Figure 2. Screenshot of our free FI Calculator. The household in our case study above reaches FI in 24.7 years, nearly 12 years earlier than in the baseline scenario, thanks in part to a better budgeting method.

The key point it that your budgeting method is not a minor administrative detail. It's the mechanism that either makes a higher savings rate possible or doesn't. Choosing the right approach is one of the highest-leverage decisions in your FI journey.

👉 Want to run your own numbers? Use our free FI Calculator (email unlock) to model how your savings rate—and your budgeting method—affects your exact retirement date.

From my own experience, getting the budgeting method right was one of the most impactful changes in our FI journey. For years, like most people, I just saved whatever was left—which wasn't much. It wasn't until I discovered FIRE (Financial Independence, Retire Early) that I got serious about expense tracking and, more importantly, switched to a Pay-Yourself-First approach—one of the seven budgeting strategies presented in this article. Automating that transfer on salary day—before anything else could get in the way—was probably the single habit that has most accelerated our path to FI.

Why Budgeting Matters: 7 Functions Beyond Expense Tracking

Budgeting is often reduced to “tracking where your money goes.” But a well-designed budget has more functions than that—especially for someone pursuing Financial Independence. Before going into the different budgeting approaches, here are seven functions a good budget should serve, each of which supports your path to FI:

Planning: A budget presents us with a clear picture of income and expenses, providing genuine control over our financial direction rather than reacting to what’s left at the end of the month. For FI pursuers, this means knowing your exact savings rate and how it relates to your timeline to early retirement.

Prioritisation: Budgeting forces you to distinguish between needs and wants, and allocates funds accordingly. This is a key skill behind developing a sense of frugality and intentional spending, which represent key traits for many pursuing FI.

Financial awareness: Reviewing monthly income and expenses periodically raises awareness of spending patterns that would otherwise remain largely invisible. Many people discover large saving opportunities only after looking at their numbers honestly for the first time on a piece of paper.

Goal setting: Establishing a budget provides a concrete framework for achieving financial goals—whether that’s building your first emergency fund, eliminating debt, reaching your first $100K invested, or hitting your full FI number. Without a budget, these goals would remain completely abstract, much more of an aspiration rather than actionable targets.

Emergency preparedness: Building an emergency fund is one of the first financial priorities for anyone on the journey to FI. A budget represents the mechanism that makes consistent contributions to that fund possible.

Debt management: Budgets can help prioritize debt repayment by making explicit trade-offs with other spending more visible. For FI pursuers, eliminating debt—especially high-interest debt—is critical. After all, every dollar in interest payments is a dollar not compounding in your portfolio.

Decision making: A well-maintained budget provides real data for financial decisions—whether to make a major purchase, whether to take a pay cut for more meaningful work, or whether you're on track to retire in your target timeframe. The FI journey is full of these decisions, and using real data always beats intuition.

Together, these seven functions explain why a good budget is about much more than just tracking spending. The question is not whether to budget, but which approach produces the best result for your specific situation.

The 7 Budgeting Strategies: Explained and Ranked for FI

There is no universally right budgeting method—the best one is the one you'll actually maintain. For most people pursuing FI, that means finding the least effortful approach that still keeps savings rate non-negotiable.

Below we present each of the seven most common budgeting methods and techniques. The seven strategies are: Traditional Budgeting, Envelope Budgeting, the 50/30/20 rule, Zero-Based Budgeting, Pay Yourself First, Percentage-Based Budgeting, and Digital Budgeting Apps. For each one I'll explain how it works in practice, what its strengths and weaknesses are, and how well it actually serves someone pursuing FI.

1. Traditional Budgeting

FI Rating: ⭐⭐

What it is: Traditional budgeting assigns fixed amounts to different expense categories (Table 1)—housing, food, transport, entertainment, and so on—based on your income and financial goals. At the end of each month, the idea is that you’ve managed to stay within each category and ideally have something left over to save.

How it works in practice: You start out by listing all your sources of income and all your expected expenses, then allocate specific amounts to each category. For example: your rent is $1,500, your groceries $500, your transport $400, and so on. You work through every line until your income is distributed. Savings represents the final line—with whatever is left after the other categories have been funded.

The FI problem: This is precisely where traditional budgeting fails to align with the FI-focused saver. By treating savings as something residual—what remains after spending—we are implicitly making savings our lowest priority. In practice, unexpected expenses, lifestyle creep, and simple human nature mean that “what’s left” is sometimes very small or nothing at all. The traditional budget is suited to avoiding complete financial chaos, but it’s poorly suited in my view to build wealth aggressively.

Pros:

Provides a clear, structured breakdown of all expenses

Easy to understand and implement

Helps identify overspending in specific categories

Cons:

Treats savings as an afterthought—it’s a passive system by design

Does not encourage aggressive wealth-building

Requires monthly discipline and effort to maintain and track each category

Best for: Someone new to budgeting who needs to get basic control over spending before optimising for savings rate.

Table 1. Conceptual example of Traditional Budgeting.

2. Envelope Budgeting

FI Rating: ⭐⭐

What it is: Envelope budgeting divides your income into either physical or virtual “envelopes” that are specific to different spending categories. When the envelope is empty, spending in that category stops for the rest of the month. Originally, it was a cash-based system, but modern versions can use bank sub-accounts or dedicated apps to create virtual enveloped for groceries, entertainment, transport, and more.

How it works in practice: At the start of each month, you allocate your income across envelopes based on your planned spending. If your grocery envelope has $400 and you spend $380, you have $20 left—which can roll over or be transferred to savings. If you spend $420, you've overspent and need to take from another envelope.

The FI problem: Envelope budgeting is excellent for spending control, which is genuinely valuable. But like traditional budgeting, it is fundamentally a spending management tool rather than a wealth-building tool. The emphasis is to avoid overspending in categories, not on maximising the amount flowing into savings and investments. Unless you deliberately create a "savings envelope" and treat it as non-negotiable, the method does little to accelerate your FI timeline.

Pros:

Highly tangible and psychologically effective at limiting overspending

Excellent for people who struggle with impulse purchases

Digital versions add flexibility and real-time tracking

Cons:

Inconvenient in a largely cashless world

Does not inherently prioritise savings or investment

Can feel rigid and time-consuming to maintain

Best for: People who have a specific overspending problem in certain categories and need a concrete mechanism to limit it.

Table 2. Conceptual example of Envelope Budgeting.

3. 50/30/20 Budgeting

FI Rating: ⭐⭐⭐

What it is: The 50/30/20 rule, often attributed to US Senator Elizabeth Warren, allocates your after-tax income into three broad categories: 50% to needs (housing, food, utilities, transport), 30% to wants (dining out, entertainment, travel), and 20% to debt repayment and savings. We cover it in detail in a dedicated article:

👉 Deep dive: Can the 50/30/20 Rule Get You to Financial Independence? Here's the Math

How it works in practice: If your net monthly income is $5,000, you'd allocate $2,500 to needs, $1,500 to wants, and $1,000 to savings or debt repayment. The simplicity is the main appeal of this approach—three simple categories instead of twenty, and a clear rule for each.

The FI problem: The 50/30/20 rule is significantly better than passive saving, and as a starting point for someone with chaotic finances it can be genuinely transformative. The problem for FI pursuers is the 20% savings allocation. As Figure 1 above shows, a 20% savings rate leads to FI in approximately 37 years at a 5% real return (or 30 years assuming 7%). This is not dissimilar to a traditional retirement, not an early one. Anyone seriously pursuing early retirement needs to push well beyond 20%, typically into the 30-50% range.

That said, the method can also be valuable as a stepping stone. Someone moving from a 5% savings rate to the 20% target of 50/30/20 has already made a massive improvement. The question is whether to stay there or keep pushing.

Pros:

Simple, memorable, easy to implement immediately

Helps people who struggle to distinguish needs from wants

Better than passive saving — explicitly allocates 20% to savings

Unlike the previous approaches, does not require so much effort to maintain

Cons:

20% savings rate is too slow for early retirement goals

The 30% "wants" allocation can feel like permission to spend freely

Rigid split may not suit variable income or high cost-of-living areas

Best for: People new to intentional budgeting who want a simple framework that's better than nothing, used as a stepping stone toward higher savings rates.

Table 3. Conceptual example of 50/30/20 Budgeting.

4. Zero-Based Budgeting

FI Rating: ⭐⭐⭐⭐

What it is: Zero-based budgeting (ZBB) assigns every dollar of your income a specific purpose—expenses, savings, investments, or debt repayment—so that your total income minus your total allocations equals zero. Not zero savings, but zero unallocated dollars. Unlike traditional budgeting, which starts with expenses and saves whatever remains, zero-based budgeting starts from scratch each month—every dollar is actively assigned a job before any spending begins.

How it works in practice: At the start of each month, you begin with your income and work through every spending category deliberately, including a savings and investment allocation. The goal is that by the time you've assigned all your income, the remainder is exactly zero—meaning nothing has been left to chance or impulse. If unexpected expenses arise mid-month, you reallocate from lower-priority categories rather than simply overspending.

The FI connection: Zero-based budgeting is a significant step up from traditional or envelope budgeting because it is fundamentally intentional. Every savings contribution is a deliberate decision, not a residual one. This intentionality is what makes it FI-compatible: it forces you to consciously decide how much to invest each month, rather than letting it be determined by whatever remains after spending.

The main limitation is that ZBB on its own doesn't guarantee you prioritise savings—you could, in theory, zero out your budget by allocating everything to expenses and nothing to savings. This is why it works best in combination with Pay Yourself First (see method 5), which sets the savings allocation before the rest of the budgeting process begins.

Pros:

Eliminates passive, unintentional spending

Forces conscious decision-making about every dollar

Effective at identifying and eliminating wasteful spending

Directly supports aggressive savings rate goals

Cons:

Time-consuming—requires detailed monthly tracking

Can feel restrictive and requires consistent discipline

Less flexible when income is irregular

Best for: Motivated FI pursuers who want maximum intentionality over their finances and are willing to invest time in the process.

Table 4.Conceptual example of Zero-Based Budgeting.

5. Pay Yourself First Budget

FI Rating: ⭐⭐⭐⭐⭐

What it is: Pay Yourself First (PYF) is arguably the single most powerful budgeting method for FI pursuers. The concept is very simple: immediately upon receiving your income, you transfer a predetermined amount to savings or investments. This happens before paying any bills, before buying groceries, and before anything else. You then live the rest of the month on what remains. It ensures you lock in your desired savings rate.

How it works in practice: Suppose your net monthly income is $5,000 and you've decided to save 30%, because you want a timeline to early retirement of around 24 years. On the day your salary arrives, $1,500 is automatically transferred to your investment account. The remaining $3,500 is what you live on for the rest of the month. Bills, groceries, entertainment—everything comes from that $3,500. There is no decision to be made about whether to save or not that month—it was already done for you automatically.

Why it works so well for FI: PYF succeeds because it removes the behavioural friction that defeats most saving strategies. Under traditional budgeting, savings is an act of willpower where you have to consciously choose not to spend money that's sitting in your account. PYF eliminates that choice by making the money unavailable in the first place. Out of sight, out of mind, and compounding in your portfolio.

This method also directly embeds your savings rate into your financial system. Every month, regardless of what else is happening in your life, a consistent percentage of your income flows into investments.

The method also aligns naturally with the FI goal of increasing your savings rate over time. Once you've adjusted to living on 70% of your income, you can gradually increase the automatic transfer to 31%, then 32%, and so on, using the 1% Savings Method principle—gradual, painless increases that compound dramatically over time.

Pros:

Automates savings and removes the willpower requirement entirely

Directly sets and enforces your savings rate

Extremely simple to implement once the automation is set up

Works with any income level

Cons:

Requires discipline to live within what remains after savings

May require initial expense optimisation to make the numbers work

Doesn't provide a framework for how to allocate the remaining spending budget

Best for: Anyone serious about FI, at any income level. This is the foundation method that all FI pursuers should implement first.

Table 5. Conceptual example of Pay-Yourself-First Budget.

6. Percentage-Based Budgeting

FI Rating: ⭐⭐⭐

What it is: Percentage-based budgeting allocates fixed percentages of your income to different expense categories—rather than fixed dollar amounts. Unlike the 50/30/20 rule, the percentages are set by the individual based on their own goals and priorities. For example, you might allocate 35% to housing, 15% to food, 10% to transport, 20% to savings, and 20% to discretionary spending.

How it works in practice: Because allocations are percentages rather than fixed amounts, this method automatically scales with income fluctuations. If you earn more one month—say, from a bonus or as a result of freelance work—your savings allocation increases proportionally without any manual adjustment. Similarly, if income drops, all categories scale down together.

The FI connection: Percentage-based budgeting is more FI-compatible than traditional budgeting because it explicitly includes savings as a category, and because the percentage approach naturally accommodates income growth—meaning the absolute amount flowing into savings and investments automatically increases with your income, without any manual adjustment. This is a useful feature for anyone on a rising income trajectory who wants to avoid some of the pitfalls of lifestyle inflation.

The limitation is that the percentages themselves are arbitrary and may not be set aggressively enough to drive meaningful FI progress. Without the discipline of Pay Yourself First, the savings allocation can still end up being optional or under-funded in practice.

Pros:

Scales automatically with income changes—good for variable earners

Flexible and customisable to individual priorities

Includes savings as an explicit, visible category

Cons:

Percentages may not be set aggressively enough for FI

Without automation, savings can still be deprioritised

Less behaviorally effective than Pay Yourself First

Best for: Freelancers, self-employed people, or anyone with variable income who needs a flexible framework that scales with earnings.

Table 6. Conceptual example of Percentage-Based Budgeting.

7. Digital Budgeting Apps and Tools

FI Rating: ⭐⭐

What it is: Digital budgeting apps—such as YNAB, Copilot, Monarch Money, or country-specific equivalents—use software to track expenses, categorise spending automatically, set budget limits, and provide insights into financial habits. Many sync directly with bank accounts and credit cards to capture transactions in real time.

How it works in practice: You connect your bank accounts to the app, set spending targets for each category, and the app tracks your progress automatically throughout the month. Most apps provide dashboards showing where you are relative to your budget, alerts when you're approaching category limits, and monthly summaries showing trends over time.

The FI problem—apps are tools, not strategies: A budgeting app is not a budgeting strategy—it's a technology layer that sits on top of one. YNAB, for example, is built on a zero-based budgeting philosophy, but the app itself is the delivery mechanism, not the approach. Using an app doesn't tell you how to allocate your income or how much to save; it helps you track whether you're following through on a strategy you've already defined.

Many people download a budgeting app, feel productive for a few days, and then abandon it because the app told them they were overspending but didn't give them a framework for changing that. The strategy has to come first. The better way to go is to pick your method from options 1-6 above, then choose an app to help you implement and track it.

Pros:

Excellent real-time visibility into spending patterns

Automation reduces manual tracking effort significantly

Can surface surprising insights about where money is going

Many offer FI-specific features like net worth tracking and investment monitoring

Cons:

Not a strategy—tracking doesn't change behaviour on its own

Some popular apps have significant subscription costs

Requires initial setup and ongoing engagement to remain useful

Best for: Anyone, as a support layer on top of whichever strategy from this list they've chosen to implement.

Now that we've covered all seven methods individually, here's how the two strongest ones work together, and exactly how to implement the combination.

The Winning Combination: Pay Yourself First + Zero-Based Budgeting

My personal favourite for anyone pursuing Financial Independence is to combine Pay Yourself First with Zero-Based Budgeting. These two methods are complementary in exactly the right way: PYF handles and locks in the most important decision—how much to save—by automating it before any spending decisions are made. Then ZBB handles everything that follows by ensuring the remaining budget is allocated intentionally rather than spent by default.

Here's how the combination works in practice:

Step 1 — Set your savings target. Decide what percentage of your net income you want to save and invest each month. The savings rate table earlier in this article shows exactly how different targets map to your FI timeline. If you're new to this, start with whatever feels achievable—even 15% is a significant improvement over passive saving. Use The Good Life Journey’s FI Calculator to see how different savings rates affect your timeline, which makes the target feel concrete rather than arbitrary.

Step 2 — Automate the transfer. Set up an automatic transfer from your current account to your investment account for the day your salary arrives. This is the Pay-Yourself-First step: the money is gone before you have a chance to spend it. Most banks allow scheduled transfers and most investment platforms allow regular contribution direct debits.

Step 3 — Zero-base the remainder. With your savings already handled, open a fresh budget and allocate every remaining dollar to specific categories—housing, food, transport, subscriptions, dining out, and so on—until the remainder is zero. This step ensures intentional spending and that impulse buying is largely left out of the equation.

Step 4 — Review and increase savings rate gradually. At the end of each month, review the zero-based budget. Where did you overspend? Where did you underspend? Over time, use the 1% Savings Method to gradually increase your automatic savings transfer—adding 1% per month until you reach your target rate. Small, consistent increases are barely noticeable in daily life but compound strongly over time.

This gradual approach is especially powerful for people who feel they arrived late to the FI journey—those in their late thirties or forties with mortgages, families, and established spending habits that are hard to change overnight. The gradual approach of PYF + ZBB makes significant savings rate improvements achievable without requiring the dramatic overnight sacrifice that puts many people off pursuing FI altogether.

Choosing your budgeting method is one of the highest-leverage financial decisions you'll make—the paths lead to very different destinations. Photo by James Wheeler on Pexels.

Which Budgeting Strategy Is Right for You?

Because not everyone is in the same situation, the “right” budgeting method depends on where you are in your financial journey. Consider the following framework to identify your starting point and where you ideally want to get to.

| Your Situation | Start With | Next Step |

|---|---|---|

| No budget — spending feels chaotic | 50/30/20 | Move to Pay Yourself First once stable |

| Have a budget but savings is inconsistent | Pay Yourself First | Automate immediately — highest single impact |

| Want maximum intentionality over every dollar | Pay Yourself First | Add Zero-Based Budgeting on top |

| Variable or irregular income | Percentage-Based | Apply Pay Yourself First within it |

| Overspending in specific categories | Envelope Budgeting | Use as temporary fix while building PYF discipline |

Regardless of which method you choose, a digital budgeting app can add useful visibility and reduce the manual effort of tracking your expenses.

Final Thoughts: From Passive to Intentional

The most important takeaway from this article is this: the best budgeting strategy for Financial Independence is whichever one allows you to shift from passive saving (“spend everything, then save what’s left”) to intentional saving (“save first, spend what remains”).

For most people, that shift is best achieved through a Pay-Yourself-First approach. On top of that, for those who want maximum control over every dollar, combining it with Zero-Based Budgeting adds another layer of intentionality. For beginners, the 50/30/20 rule can be a solid, initial stepping stone.

In the end, what matters most is not which specific method you choose, but that you actually choose one and implement it consistently. Even a modest improvement in savings rate, sustained consistently, will do more for your FI timeline than almost any other financial decision you make.

If you enjoyed this guide, here are some next steps:

👉 For the full FI framework, see our complete guide to Financial Independence

👉 Use our FI Calculator to see how your savings rate affects your FI date (email unlock)

👉 Browse 130+ articles on FI, investing, work, and lifestyle at The Good Life Journey

👉 Subscribe for weekly insights—one-click unsubscribe

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I am not a financial adviser, and this content is for informational and educational purposes only. Please consult a qualified financial adviser for personalized advice tailored to your situation.

Check out other recent articles

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Frequently Asked Questions (FAQs)

-

The combination of Pay Yourself First and Zero-Based Budgeting is the most effective for FI. Pay Yourself First automates your savings before any spending decisions are made; Zero-Based Budgeting ensures the remaining income is allocated deliberately. Together they transform saving from passive to intentional—which is the single most important shift in the FI journey.

-

The seven most common budgeting methods are: Traditional Budgeting, Envelope Budgeting, the 50/30/20 rule, Zero-Based Budgeting, Pay Yourself First, Percentage-Based Budgeting, and Digital Budgeting Apps. Each has different strengths—see the comparison table above for a quick overview of which suits which situation.

-

Zero-based budgeting assigns every dollar of your income a specific purpose—expenses, savings, investments—so that income minus allocations equals zero. The goal is not to have zero savings, but to have zero unallocated dollars. Every pound or euro has a job, which eliminates passive, unintentional spending.

-

The 50/30/20 rule allocates 50% of net income to needs, 30% to wants, and 20% to savings or debt repayment. It's a useful starting point for building budgeting habits, but the 20% savings rate it prescribes leads to FI in roughly 30 years at a 7% real return—essentially a traditional retirement rather than an early one.

-

Pay Yourself First is the most effective single method for building savings, because it automates the saving decision before any spending can occur. By treating savings as a non-negotiable first allocation rather than a residual, it systematically builds wealth regardless of willpower or discipline in the moment.

-

Start by assessing your current situation: if finances are chaotic, begin with 50/30/20. If savings is inconsistent despite having a budget, switch to Pay Yourself First immediately. If you want maximum control and are comfortable with detailed tracking, add Zero-Based Budgeting on top. See the decision framework section above for a more detailed guide.

-

Yourself First combined with the 1% Savings Method is particularly effective for people in their late thirties or forties with established spending commitments. Rather than requiring dramatic overnight sacrifice, it uses gradual, automated increases in savings rate that compound significantly over time without feeling disruptive.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles: