Best and Worst US & Canadian Cities for Financial Independence (2026 Rankings)

Waikīkī beach, Honolulu. Photo by Spenser Sembrat on Unsplash

Reading time: 7 minutes

Quick answer — Which US and Canadian cities are best for Financial Independence?

Based on salary-to-cost-of-living ratios, Atlanta, Seattle, and St. Louis surprisingly outperform more glamorous options. San Francisco's high salaries are offset by even higher costs, while Honolulu, Miami, and New York rank among the worst for building wealth quickly. Canadian cities generally lag US cities, with Victoria and Vancouver performing worst in the dataset.

What you'll get in this article

✔ A ranked comparison of 51 US and Canadian cities by Financial Independence (FI) potential

✔ The salary vs cost-of-living data behind each ranking

✔ Why some high-salary cities (San Francisco, New York) underperform for FI

✔ The best and worst Canadian cities for the accumulation phase of FI

✔ An interactive tool to compare your own city against the full dataset

TL;DR — Best US & Canadian Cities for FI 🏙️

🥇 Top performers: Atlanta, Seattle, St. Louis—high salaries, reasonable costs

💸 Worst performers: Honolulu, Miami, New York—high costs eat the salary advantage

🍁 Canada lags overall—Victoria and Vancouver are the weakest in the dataset

📊 The key metric: savings rate potential, not absolute salary

🌍 Relocating during the accumulation phase can cut years off your FI timeline

🔧 Use the interactive tool below to compare your city directly

Analyzing the Best US and Canadian Cities for Financial Independence

(Edit: based on this article, we have developed a global tool to identify the best cities for pursuing FI. It considers 312 different cities across 106 countries.)

Most people assume the best cities for building wealth are the ones with the highest salaries—New York, San Francisco, or Los Angeles. The data tells a different story. When you factor in cost of living, Atlanta outperforms New York, St. Louis beats San Francisco, and Vancouver is one of the worst cities in the dataset for reaching Financial Independence quickly.

In this article, we rank 51 US and Canadian cities by their salary-to-cost-of-living ratio—the metric that actually determines how fast you can build wealth and reach Financial Independence (FI). For readers thinking about the other side of the journey—where to retire once FI is reached—see also our complete guide to geographic arbitrage and retiring abroad.

51 US and Canadian Cities Ranked for Financial Independence in 2026

Savings Rate: The Key to Achieving Financial Independence Faster

In previous posts, we highlighted that your savings rate—calculated as the percentage of your net take-home income that you regularly save and invest—is the most critical factor for achieving financial independence.

Online calculators can help you estimate how long it will take to retire early based on your savings rate and lifestyle choices (for example, you can use our FI Calculator—free via email unlock). The main point, as shown in Figure 1 below, is that your savings rate has a disproportionate, non-linear impact on the time that is required to reach Financial Independence.

Reducing your expenses not only increases your monthly savings but also decreases the overall portfolio amount you need to target, greatly speeding up your journey to financial freedom. This dual effect creates a non-linear relationship between your savings rate and the years needed to achieve FI, as we explore in depth in our complete guide to Financial Independence.

Figure 1: Non-linear relationship between your savings rate (X axis) and your timeline to reaching financial independence (Y axis). Source: Networthify.

How We Ranked US and Canadian Cities for Financial Independence

To improve your savings rate and fast-track financial independence, consider strategies like cutting living costs or increasing your income in cities with favorable economic conditions. Factors such as your net take-home pay and the local cost of living clearly play a significant role in how quickly you achieve FI. Relocating to cities with higher salaries and lower living costs can be a game-changer for achieving Financial Independence and retiring early.

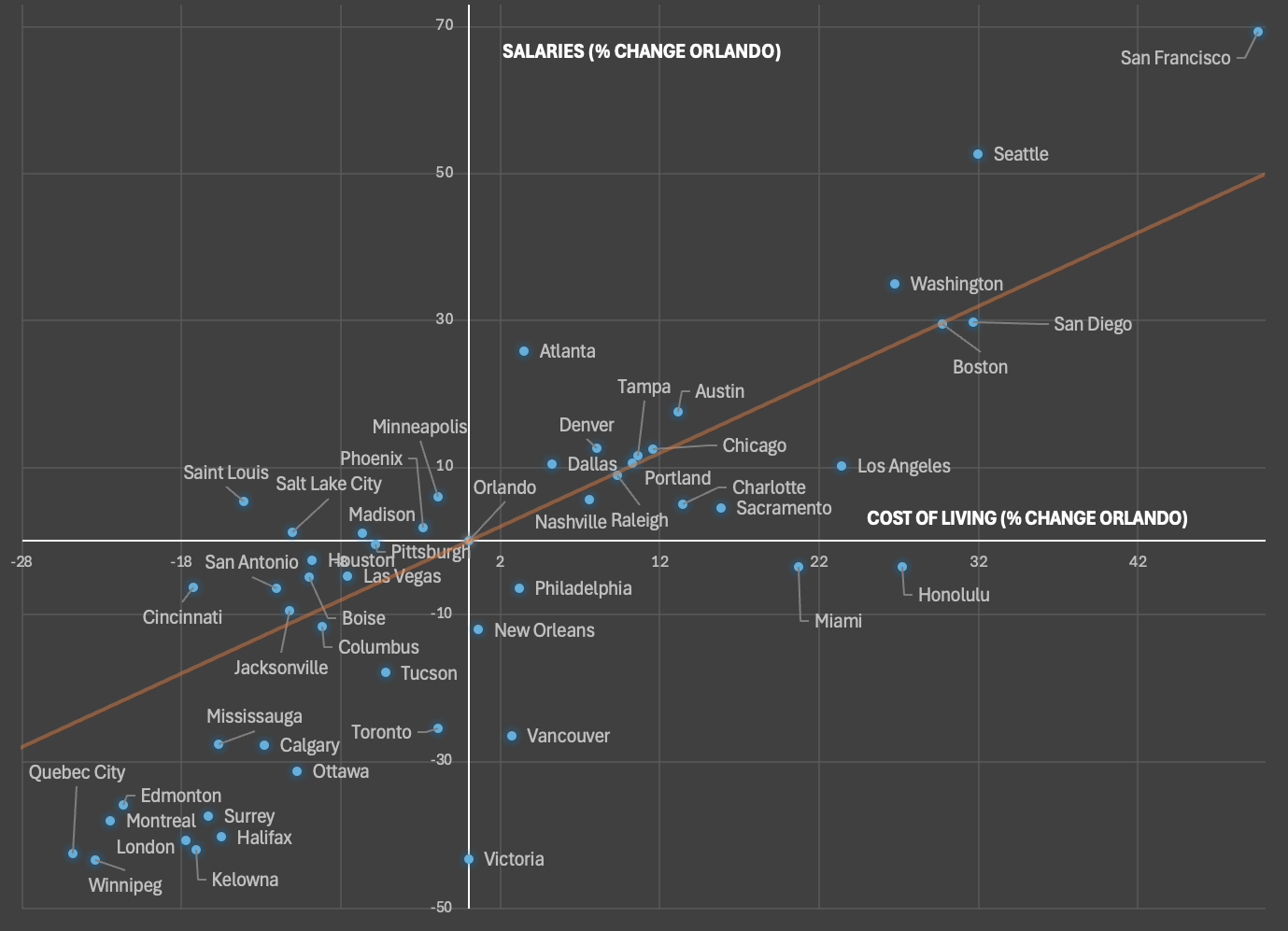

For this analysis of cities in the US and Canada, we relied on cost of living and after-tax salary data sourced from Numbeo, a trusted resource for global data. Our assessment spans 51 cities. To explore differences across cities, we employed a comparative methodology using Orlando as the reference point (0,0 in Figure 2).

As shown in Figure 2 below, the X-axis represents the cost of living in each city as a percentage of Orlando’s, while the Y-axis shows the net average salary relative to Orlando. For example, San Francisco’s cost of living is 49.5% higher than Orlando’s, while Minneapolis offers salaries that are 6.0% higher on average. Conversely, Toronto has salaries that are 25.4% lower.

The red line in the chart serves as a benchmark, showing which cities have a salary-to-cost-of-living ratio comparable to Orlando’s Financial Independence potential. For instance, Portland, Tampa, Chicago, or Boston fall on or are very close to the red line: despite the net average salary being a certain percentage higher than the one found in Orlando, its cost of living is also higher by the same percentage.

This suggests that the Financial Independence journey in the locations falling on the red line would be roughly comparable to each other. Otherwise, countries falling above the line would be considered more advantageous in terms of pursuing FI than Orlando, due to a better salary-to cost of living ratio.

Figure 2: Identifying suitable cities to pursue Financial Independence from the perspective of someone living in Orlando (0,0 in the graph). The X axis depicts the cost of living difference (%) in relation to Orlando’s cost of living. They Y axis presents the net average salary difference (%) in relation to Orlando’s salary. In general, countries situated above the red line are—in theory—better performers than Orlando for these two variables. You can enter your own city and re-run the results in our free tool below:

Top US and Canadian Cities to Pursue Financial Independence in 2026

As observed in Figure 2 above, Orlando is not a very optimized location for pursuing FI. From the perspective of someone living in Orlando, there are 23 cities in the dataset were it may be, on average, easier to pursue Financial Independence: the top locations were Atlanta, Seattle, San Francisco, St. Louis, with net average salaries 26%, 53%, 69%, and 5% higher than in Orlando. In contrast, the cost of living in Atlanta, Seattle, and San Francisco was only 3%, 32%, and 50% higher, respectively, than in Orlando. In St. Louis, the cost of living was 14% lower.

The least favorable cities in the US for achieving FI were Honolulu, New York, Miami, and Los Angeles. In Honolulu and Miami the cost of living was 27% and 21% higher than in Orlando, yet the salaries were 3% lower in both locations. Clearly, here we see that these are retirement destinations, not ideal locations (on average) for the accumulation phase of FI. Los Angeles and New York displayed cost of living that were, respectively, 23% and 58% higher than Orlando, yet their salaries were only 10% and 28% higher, respectively.

Canadian cities, on average, rank lower than US cities in terms of financial independence potential. The cities closest to the benchmark (red line in Figure 2) were Mississauga, Edmonton, Calgary, and Montreal. These would be the cities where, on average, the ratio salary-to-cost of living appears to show most promise. In contrast, Victoria and Vancouver are the worst performing Canadian cities in the dataset. Victoria’s cost of living is exactly that of Orlando, but with 43% lower salaries. Similarly, Vancouver’s cost of living is 3% higher than Orlando, but its salaries are 27% lower.

Key Factors Beyond Salaries and Costs When Choosing a City

As we reminded in previous posts, there are many other important factors to take into account when choosing a country or city to pursue FI. This post presented an approach for identifying a preliminary set of locations where it may be easier to achieve financial independence. However, when considering relocating to a different place please remember that there are many other factors at play that should be assessed, summarized in Table 1.

Table 1: Example of variables to consider when deciding to move to another country in search of better economic opportunities.

| Category | Variables |

|---|---|

| Economic Variables |

- Job opportunities and industry relevance - Currency stability and exchange rates - Inflation rates and economic stability |

| Legal and Political Environment |

- Political stability and freedom - Ease of obtaining work or residency visas - Legal protections for expats and workers - Property rights and investment opportunities |

| Quality of Life |

- Healthcare quality and affordability - Education system - Safety and crime rates - Air and water quality |

| Cultural and Social Factors |

- Language barrier and availability of resources for non-native speakers - Cultural compatibility and social norms - Community and networking opportunities for expats - Food and cuisine variety |

| Infrastructure and Accessibility |

- Transportation systems and connectivity - Availability of technology and internet - Proximity to other countries for travel |

| Personal and Family Considerations |

- Access to healthcare for family members - Availability of recreational activities and lifestyle preferences - Work-life balance culture - Climate and weather preferences |

| Financial System and Opportunities |

- Banking systems and ease of transferring money - Investment opportunities and regulations - Access to affordable housing and utilities - Social security or retirement benefits for residents |

| Cultural Tolerance and Diversity |

- Acceptance of diverse cultures, religions, and lifestyles - Religious freedom and tolerance |

| Taxation and Residency Benefits |

- Double taxation treaties with your home country - Retirement benefits or tax incentives for expats |

| Future Considerations |

- Long-term prospects for citizenship or permanent residency - Stability of political policies and leadership - Opportunities for personal and professional growth |

Conclusion: Best Cities for Accelerating Financial Independence

We presented a simple yet effective method for identifying the best cities to fast-track progress toward FI. By analyzing publicly available data from Numbeo, we compared the cost of living and average net salaries across 51 cities in the US and Canada.

The objective was to equip readers with insights to help them make informed decisions about relocating during the accumulation phase of their FI journey. For the full framework on what the accumulation phase involves—including savings rates, investment strategy, and FI number calculation—see our FI guide.

It is possible to replicate this analysis for your own city or country by using Numbeo data and tailoring it to your specific circumstances. Alternatively, use the charts above to get a general sense of how other cities compare to yours.

💬 Is your city on the list? Where does it rank—and would you consider relocating to accelerate your FI timeline? Let us know in the comments.

If this was useful, here are some next steps:

👉 Estimate your FI timeline with our free FI Calculator (email unlock)

👉 For the full framework on retiring abroad and geographic arbitrage—destinations, taxes, and timelines—see our complete guide to geographic arbitrage and retiring abroad

👉 Subscribe for weekly insights on money, FI, and living well—one-click unsubscribe

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I am not a financial adviser, and this content is for informational and educational purposes only. Please consult a qualified financial adviser for personalized advice tailored to your situation.

San Francisco’ problems are well known, but it does have outstanding salaries in some sectors. Would you be willing to relocate for 10 years to accelerate FI? Photo by Natalie Chaney on Unsplash.

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Check out other recent articles

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles: