FIRE and Housing FOMO: 10 Reasons I’m Still Renting While others around me Buy

Everyone’s dreamhouse looks different—what’s it like for you? Beach in Cape Town, South Africa. Photo by Taryn Elliott on Pexels.

Reading time: 6 minutes

Quick answer:

Housing FOMO is the sense that you’re falling behind because you haven’t bought a home while others around you have. But when buying would push back your Financial Independence (FI) timeline, the solution is to separate status pressure from your real goals. Check the rent-vs-buy math, estimate the years of early retirement delay, and use simple mindset guardrails to stay intentional and avoid impulse decisions.

What you’ll get from this article

✔ A clear definition of housing FOMO (and why it spikes in your 30s)

✔ A quick rent-vs-buy benchmark (the 5% rule) to sanity-check real estate prices

✔ A simple way to estimate “how many years a house costs you” on the path to FI

✔ 10 practical tactics (numbers + mindset) to stay calm while others around you buy

✔ When buying can make sense—even for FIRE

TL;DR — Housing FOMO 🏠😬

🏠 Housing FOMO = fear you’re missing out by not buying when peers do

⏳ If buying delays FI, your job is to protect time freedom—not win a status race

📏 Use the 5% rule to sanity-check whether buying is financially reasonable

🧮 Estimate the years of FI delay a home purchase could create

🌱 Practice gratitude for your current lifestyle to reduce comparison pressure

🧭 Keep flexibility and optionality as core FIRE advantages

How to Avoid Housing FOMO and Stay on Track to Financial Independence

Watching friends and family buy homes can spark powerful doubts when you’re renting and pursuing Financial Independence (FI). In this post I share the numbers, lifestyle trade-offs, and ten practical tactics that help me resist the pressure to “buy because everyone else is buying”—so you can stay focused on freedom and your own FI timeline.

Why Housing FOMO Hits Hard in Your 30s (Even If Renting Works)

In my late thirties, after a six-year path to Financial Independence, I find myself surrounded by friends, colleagues, and neighbours purchasing their first homes. Some of them are settling into city flats, while others are heading out for the outskirts or countryside.

At weekend gatherings, their talk of mortgages and dream renovations sometimes trigger a quiet sense of FOMO—fear of missing out—that is increasingly hard to ignore. In practice, it often shows up as house-buying pressure, where I continuously catch myself thinking to myself: “Are we making a mistake by renting?”

Both my parents and in-laws, who grew up believing homeownership is an important milestone of life and the ultimate badge of adulthood, sometimes (gently) question whether we’re considering to buy. While I understand my friend’s and family’s perspective, it creates for me an emotional tug between optimizing for Financial Independence and early retirement and the natural urge to follow my peers.

I think this tension is further sharpened by uncertainty—I’m in the midst of a career change and exploring new ways to work that provide a greater sense of satisfaction and work-life balance. Buying a home at this point would certainly be a major financial commitment just as my professional life is in flux—perhaps not the best idea. And yet, when everyone else seems to be going down the ownership path, it’s really difficult to stay the course and remember why we chose this different path.

In today’s post I want to share the discipline and the competing arguments that help me stay the course—the thought process, the financial logic, and the mindset shifts to keep house-buying FOMO at bay—so major decisions support long-term Financial Independence and lifestyle goals, rather than short-term peer pressure.

Perhaps you dream of an English cottage by the sea? Polperro, Looe, UK. Photo by Martina Jorden on Unsplash.

The 5% Rule (Rent vs Buy) as a Quick FOMO Filter — Germany Example

I use the well-known 5% rule for renting vs buying a house as a quick benchmark. It helps to avoid apples-to-oranges comparisons by considering certain home ownership costs that you don’t have when you rent—property taxes (the rule assumes 1% per year), house maintenance costs (1%), and the opportunity cost from the capital you could otherwise invest (3%). Although this 5% rule can be tailored to the tax realities of individual locations, it serves as a good starting point.

Here’s an example of how to use it. We pay roughly €2,000 a month (€24,000 annually) for our four-room city flat in a mid-sized city in Germany. According to the 5% rule, a comparable purchase for this flat would be about €480,000 (€24,000/0.05). According to this simple rule of thumb, if flats were being sold for €300,000 in our area, it would be financially wise to buy, whereas if a comparable flat were priced at €600,000 it would be better to rent from a purely financial standpoint.

Here is the thing: we regularly see comparable flats to ours on the market for over €900,000. Under these circumstances and according to the benchmarking rule, renting is not “throwing away money”; it is by far the more sensible decision if we choose to stay in our neighbourhood. The “comparable rent” for this property price would be €3,750 per month—which is incredibly steep—nearly twice what we pay.

This is why the key question isn’t to consider “renting vs buying” in the abstract—it’s renting vs buying at today’s prices in your exact neighborhood (assuming you’re happy were you live).

Perhaps you dream of restoring a chateau in the French countryside? Dives-sur-Mer, France. Photo by Baptiste Pilot on Unsplash.

City vs Countryside: Would Moving Outside the City Delay or Speed Up FI?

But what about moving elsewhere? We probably wouldn’t want to move to a worse neighbourhood just for the sake of buying a house, but what about somewhere outside the city or perhaps somewhere even more rural? In a previous post about a “dream farmhouse”, I estimated that buying could delay reaching Financial Independence by four-to-five years for us.

This is not too much if that is really your dream. But the point is being clear-eyed that buying still sets you back financially compared to renting. These decisions aren’t just about extra money; they also affect how long you need to work—whether full-time or part-time—and how much time you spend with your kids, travel, and other life experiences.

City life carries its own blend of pros and cons. On the plus side, we are lucky that we can cycle from here to rivers and lakes, avoid car ownership, and live a relatively green and active lifestyle. There are also tons of activities and cultural events around us.

Yet the benefits are not all one-way. Air pollution and the subtle stress of city life can offset some of those health benefits, and there is also the well-researched quiet fatigue that comes from background noise and hurried interactions.

In relation to housing, living in the city you normally lack the private outdoor space of your own. Owning a house might create a feeling of permanence and personal space that is tricky to match with renting a flat. Whenever we travel, the contrast between our urban area and the open spaces elsewhere makes us wonder what life might be like beyond the city limits.

Perhaps you dream of a stone-house retreat on a lake? Rifugio Lago Nambino, Madonna di Campiglio, Italy. Photo by Vincentiu Solomon on Unsplash.

Temptation of Rural Living: Germany’s Countryside and Danish Villas

Occasionally, we feel the quiet pull of the countryside. Travelling recently in Denmark and northern Germany, I noticed charming villas and farmhouses selling for a fraction of what similar spaces would cost in our region—whether a flat in the city or a house in the outskirts. These rural properties highlight the classic city vs countryside living dilemma many FIRE seekers face.

As we covered in detail in a previous post, in Denmark you can find €300,000 seaside houses with land in dreamy environments and tightly-knit communities. It’s easy to picture ourselves living a slower pace by the sea with our kids growing up outside and close to nature.

The rural upsides feel very real to me: a slower, less rushed rhythm, stronger neighbourly ties, and children learning hands-on skills—gardening, building, and observing the seasons. Such a childhood could build resilience and a deep connection to nature. And for the parents, life may feel more intentional and less driven by schedules and screens.

Yet rural living carries trade-offs too. Older kids may need to be driven places—public transport is often sparse. Job opportunities and cultural offerings can be limited, and daily errands may require a car.

It’s clear that these layered pros and cons make the decision to buy outside the city versus rent inside it far more difficult than a simple spreadsheet exercise. Ultimately, it’s about weighing the lifestyle you want both now and in the years to come.

If you don’t mind the cold, perhaps you dream of a home in some Scandinavian country, surrounded by stunning scenery? Source: StefanoZaccaria on iStock.

Parenting and Lifestyle Choices Once You Reach Financial Independence

A question I keep circling back to is what happens once we reach FI? My partner’s job is stable now, but it’s becoming increasingly clear that she likely doesn’t want to stay in it forever. Financial Independence isn’t just about quitting work—but having the choice to pivot. If we both were to crave a slower lifestyle and didn’t need our jobs, why not try the move to the countryside?

Children adapt far better than we sometimes fear. Ultimately, what matters most for their well-being is consistent love, time, and emotional support from their parents. Whether it’s in a bustling city or a quiet village, kids thrive when their environment is stable and nurturing. A move after FI, planned and communicated well, could be an enriching family adventure rather than a disruption.

For families on the path to FIRE, this flexibility to move later can be part of a long-term plan. So, while career disruption may be a strong disadvantage today, in a few years time it might not be. After reaching FI, these lifestyle questions and housing preferences may look different than they do today—especially if everyone around us indeed continues to leave our neighborhood to buy a house somewhere else!

But in the meantime, what can we do about this feeling of FOMO? Below are 10 different ideas to help overcome it. The idea is ultimately to make life decisions based on rational preferences, not jump on what others are doing out of fear.

10 Practical Ways to Overcome House-Buying FOMO (Numbers + Mindset)

Below are ten practical ways to quiet the urge to “buy because everyone else is buying”. Some of these are financial checks, while others are mindset shifts. Together they help keep me grounded when FOMO inevitably hits.

1. Run your own 5% rule numbers

Divide your annual renting costs by 0.05. Are property prices much higher than that value for a comparable home where you live? Chances are renting is the better financial decision—at least in many major cities in Europe. You’re definitely not throwing away money just because you are renting.

2. Track your net worth

People like to say that renting is throwing away money, but seeing your portfolio grow over time should reinforce the idea that wealth creation doesn’t need to be tied to bricks and mortar. Slow, consistent investing is the simplest path to wealth.

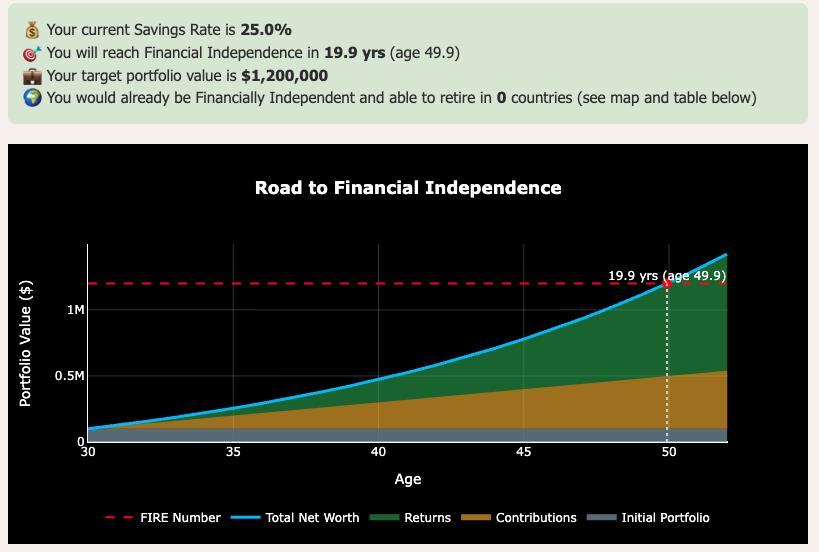

3. Estimate the “delay to Financial Independence”

Use our FI calculator—free for our email newsletter subscribers—and model how many extra years of work would a house purchase add to your Financial Independence timeline. In my “dream farmhouse” scenario, it was four to five years, but it could be much longer if you’re considering buying in the city. Understanding this relationship can highlight a powerful perspective.

Figure 1: Screenshot of our FI Calculator (free, email unlock). Enter different annual expense scenarios and model how buying vs renting affects your timeline to reaching early retirement.

4. Recognize the lock-in effect

If you are renting, you are also less limited career-wise for pivots and in terms of geographic flexibility. Of course, if you own a house you can sell it, but in practice it represents a much larger hurdle to relocating. Naming this hidden cost helps you value the freedom that renting gives you.

5. Understand other people’s motivations and financial literacy

Most people don’t invest consistently; for them buying a home represents their main “forced-savings plan”. It probably does make sense financially for them to buy to force some savings. But your situation may be very different to theirs. And, of course, for many families buying isn’t just about spreadsheets—it can be the lifestyle choice that makes them happiest even if the numbers don’t perfectly line up.

Perhaps you dream of something modern not too far from the city? Photo by Stephan Bechert on Unsplash.

6. Practice gratitude for your current setup

Go over the perks of renting. For us, it’s living in a mid-sized city we love, with access to rivers and lakes, lots of events, and the possibility of living a (mostly) car-free lifestyle. One of our weekly rituals is taking the kids to our Kleingartenverein plot—an allotment garden fifteen minutes by bike—where we grow vegetables and enjoy a private outdoor space. This reminds me we already have many of the perks of a house without the mortgage and other downsides.

7. Remind yourself you can buy later

As I mentioned earlier, I’m not opposed to buying, I just think the timing isn’t right yet. Assuming you are saving and investing, there is no reason you can’t delay a bit the home ownership decision. Of course, waiting carries the risk of rising home prices. But as long as your investment portfolio grows at a healthy long-term rate, the opportunity cost of locking money into a house often outweighs moderate property price growth.

8. Compare lifestyle costs, not just housing costs

Suburban or rural homes require a car and longer commutes. Factor in car ownership costs—at least €500 per month—and time.

9. Quantify non-financial stress

House maintenance surprises, renovation headaches, or rising property taxes are rarely captured in spreadsheets but can be very real.

10. Redefine success

Success is living your chosen life, not meeting cultural milestones set by others. Homeownership is optional, not mandatory. Remember that the best status signal of all is ultimately good health and the time-freedom granted by Financial Independence.

Perhaps you dream of retiring early abroad? Bali, Indonesia. Photo by Antonio Araujo on Unsplash.

Avoid Housing FOMO and Stay on Track to FIRE

The essence of Financial Independence is freedom of choice. By resisting the urge to buy now, we keep multiple doors open: buying a home later, renting indefinitely and staying flexible, or even relocating abroad. The working years you can save by not taking on a €800,000 mortgage can translate to more freedom. You can always choose to buy later on with the backing of a larger investment portfolio.

The real asset isn’t a house but flexibility itself. Your wealth is the time and options you preserve. FOMO loses its power once you see that freedom—not square footage—is the ultimate form of security, and that buying at the wrong time can lengthen your career and limit the work-life balance many crave for.

There are also other ways to gain exposure to real estate without buying a home at all. For investors who still want to participate in property markets while staying flexible, REITs (Real Estate Investment Trusts) can be an alternative worth exploring. And for those who do eventually buy—the question of whether to overpay the mortgage or invest the surplus each month is worth thinking through carefully. Our mortgage vs investing guide shows that the answer depends almost entirely on your interest rate.

I think it’s natural to experience housing FOMO—especially when friends and family assume buying is the only financially responsible path. But with a clear FI strategy, the numbers, lifestyle tradeoffs, and long-term vision all point towards the same conclusion: renting today can be a solid choice, not a failure.

For now, our “home” is the life we’re building, and we’re happy with our current setup. I can see us eventually buying, perhaps in the countryside or even abroad. Either way, it will be because it’s a decision that supports our values and lifestyle preferences, not because we rushed to keep up with others.

Many people follow default financial paths without a clear long-term plan—often working decades longer than they expected. Perhaps the average person should not be your benchmark for making your personal life decisions.

To be clear, I’m not against homeownership at all. In some markets the maths—after property taxes, maintenance, and the opportunity cost of tied-up capital—can still favour buying. And even where it doesn’t, choosing to own a home can absolutely be the right move for those who value the stability and lifestyle it provides.

If you enjoyed today’s article, here are some next steps:

👉 Calculate your Financial Independence timelinewith our FI Calculator (free, email unlock) and see how it changes under buying vs renting scenarios

👉 Subscribeto access free tools and our monthly newsletter with new articles and insights

👉 Explore a detailed post comparing the math on renting vs buying

💬 Have you experienced house ownership FOMO? How do you deal with it and what are your plans for the future? Please let us know in the comments below!

🌿 Thanks for reading The Good Life Journey. I share weekly insights on personal finance, financial independence (FIRE), and long-term investing — with work, health, and philosophy explored through the FI lens.

Disclaimer: I’m not a financial adviser, and this is not financial advice. The posts on this website are for informational purposes only; please consult a qualified adviser for personalized advice.

About the author:

Written by David, a former academic scientist with a PhD and over a decade of experience in data analysis, modeling, and market-based financial systems, including work related to carbon markets. I apply a research-driven, evidence-based approach to personal finance and FIRE, focusing on long-term investing, retirement planning, and financial decision-making under uncertainty.

This site documents my own journey toward financial independence, with related topics like work, health, and philosophy explored through a financial independence lens, as they influence saving, investing, and retirement planning decisions.

Check out other recent articles

Frequently Asked Questions (FAQs)

-

Housing FOMO is the anxiety that you’re missing out on stability, wealth, or “adult success” by renting while others buy. It’s social comparison plus uncertainty about future prices. Naming it helps you stop treating a lifestyle choice as a status emergency.

-

Rent is the price of housing services (shelter + flexibility). Buying also has unrecoverable costs: interest, taxes, maintenance, transaction fees, and lost investment returns on your down payment. The right question is which option is cheaper after those costs.

-

Estimate the change in monthly investable cash flow (rent vs total ownership cost) and the down payment opportunity cost. Then translate that into “years to FI” using your FI number. Even small monthly differences can compound into years.

-

The 5% rule approximates annual unrecoverable ownership costs (taxes + maintenance + capital/opportunity costs). Divide your annual rent by 0.05 to get a rough “fair buy price” for a comparable home. If market prices are far above that, renting is often rational.

-

Because peers start buying, families grow, and cultural scripts label ownership as adulthood. At the same time, careers are still flexible and uncertain—exactly when a mortgage can reduce options. That mismatch creates psychological pressure.

-

Buying can make sense if you’ll stay long-term, prices are reasonable relative to rent, and ownership meaningfully stabilizes future housing costs. It can also work if you’re not investing consistently—mortgages can act as forced savings. The “best” choice depends on goals and behavior.

-

Switch comparison from milestones to outcomes: time freedom, health, family stability, and optionality. Track your own net worth and FI progress so the story stays evidence-based. And remember: people rarely talk about the stress and costs after they buy.

-

Often yes, because FI increases flexibility: you can choose where to live without job constraints. After FI (or close to it), you can buy for lifestyle value without jeopardizing freedom. The tradeoff is price risk—but your portfolio growth may offset that.

-

Treating “buy now” as irreversible and urgent. The better move is to test: rent a countryside place for a month, try a garden allotment, or run numbers with conservative assumptions. FOMO thrives on vagueness; clarity kills it.

Join readers from more than 100 countries, subscribe below!

Didn't Find What You Were After? Try Searching Here For Other Topics Or Articles: